Top 5 Effective Ways to Get Approved for a Car Loan in 2025

Securing a car loan approval in 2025 requires preparation and strategies tailored to the evolving market. Understanding the loan application process, highlighting essential car financing tips, and improving your creditworthiness can significantly enhance your chances. This article delves into the effective ways to ensure your car loan application stands out.

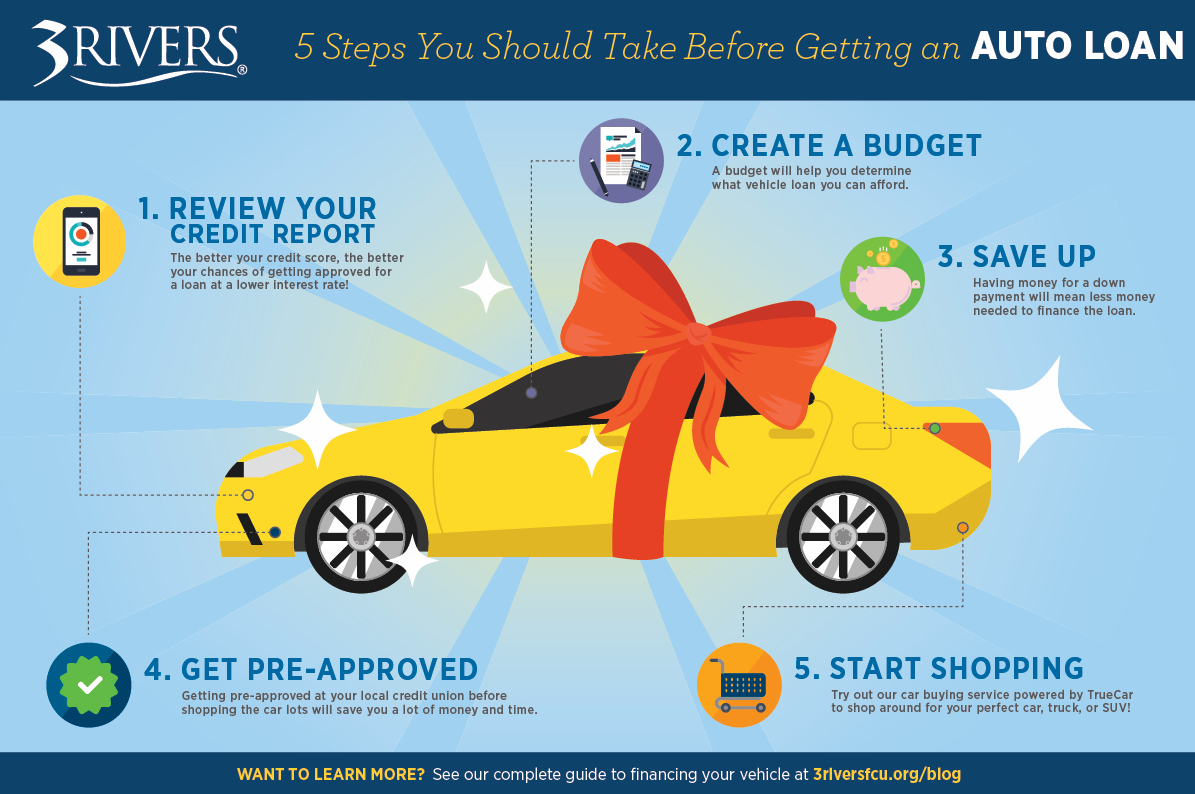

1. Improve Your Credit Score for Loan Approval

A robust credit score is one of the most crucial factors affecting your loan approval. Before applying for a car loan, take the time to **evaluate and improve your credit score**. You can achieve this by paying your bills on time, reducing existing debt, and avoiding new credit inquiries. A score of 700 or above usually attracts better interest rates for car loans. Additionally, regularly check your credit report for inaccuracies and take steps to resolve them; small discrepancies can impact your loan eligibility.

Understanding Credit Score Requirements

Every lender has different credit score requirements for car loans. Typically, those with excellent credit scores receive the most favorable terms. Familiarize yourself with what each lender demands, be it a minimum score or specific debt-to-income ratios along with open lines of credit. Take proactive measures like limiting credit inquiries and not taking on excess debt, which can help appraise your creditworthiness and influence car loan approval.

Steps for Rating Your Credit Report

To effectively rate your credit report, start by obtaining a copy from leading credit bureaus. Assess each section, taking into consideration factors like your payment history, amounts owed, and the length of your credit history. Look for **potential errors or outdated information** that could negatively affect your score. Understanding where you stand gives you leverage when discussing terms with lenders, as a solid record can enhance your bargaining strength during the car financing negotiations.

2. Required Documents for Car Loan Application

The documentation for auto financing is integral to a smooth application process. Armed with the correct documents expedites the approval process and strengthens the lenders’ trust in your financial stability. Essential documents typically include proof of identity, income verification for car loans, and residency documentation. Applicants should prepare their down payment showings, such as bank statements, which might also expedite their pre-approval.

Income Verification for Car Loan

Most lenders require proof of income to assess your ability to repay the loan. Acceptable documents include recent pay stubs, tax returns, and bank statements revealing ongoing consistent income. Presenting clear and adequate financial information may help ease the negotiation of loan terms, reinforcing your case as a reliable borrower.

Common Mistakes in Loan Applications

Applications missing critical documents or containing inconsistencies can result in delays or outright denial. Ensuring completeness in your documentation includes confirming compliance with the loan eligibility criteria necessary to strengthen your application. Take time to double-check each document to avoid common pitfalls such as mismatched income sources and inadequate residency proof, which could hinder the chances of your car loan approval.

3. Choosing the Right Lender

Selecting the right lender could mean the difference between a successful **loan approval** and a prolonged approval process. Compare rates and terms from different lenders to find one that caters best to your needs. Consider options like credit unions or local banks, which may offer more favorable conditions compared to larger banks or dealership lending. Utilizing lender comparisons can facilitate finding that best caters to your financial stability for loan approval.

Benefits of Good Credit in Choosing a Lender

Having a good credit profile enables you to negotiate better rates with lenders. You can command better interest rates, flexible terms, and sometimes even residual money-saving opportunities like waived fees. So keep your credit in peak condition before entering the negotiation phase with lenders, as having a strong credit position can further improve your overall chances of securing a better offer.

Comparing Loan Deals

Take advantage of the online tools available for comparing multiple car loan offers. Utilize auto loan calculators to assess the total cost of different financing options. This will help you understand the potential impact of various interest rates, payment frequencies, and any attached processing fees for car loans. Furthermore, engaging in negotiations with your chosen lender can allow you to refine the terms to better suit your financial situation.

4. Utilize the Pre-Approval Process

The pre-approval process allows borrowers to gauge their eligibility prior to choosing a specific vehicle. Understanding whether you qualify for financing and how much ensures you know your budget before shopping. This step not only clarifies your financial landscape but also reinforces your standing when engaging with sellers. Many times, a pre-approved borrower qualifies for better deals during car financing actions.

Advantages of Pre-Approval

The benefits of obtaining pre-approval extend beyond just knowing the potential loan amount. Importantly, it significantly accelerates the transaction process once you find the vehicle that fits your wants and needs. Pre-approved buyers often stand out to sellers and dealers, as lenders have already determined that these applicants are likely to be low-risk borrowers. Additionally, securing pre-approval can prevent the standard anxiety during car purchases and transform them into a more simplified buying experience.

Understanding Loan Terms and Agreements

Prior to signing any agreement or accepting loan terms, take time to decipher each component. Familiarizing yourself with loan terms, annual percentage rates (APR), and repayment options can save borrowers from future regrets. Clear comprehension helps avoid pitfalls caused by missed payments or negative loan characteristics such as high annual fees and hidden charges. Empty agreements can backfire dramatically, so it’s key to swagger within the details effectively.

Each of these methods fosters a proactive mindset towards understanding the landscape of securing a car loan. By implementing these strategies, getting approved for a car loan becomes leveraged by an informed process, maximizing efficiency while minimizing setbacks. For any borrower in 2025, these steps can deliver the speed and accessibility you need.

FAQ

1. What affects my car loan approval chances the most?

Your credit score and overall financial health play a paramount role in determining your car loan approval chances. Factors such as a low debt-to-income ratio and a steady income also contribute significantly. Understanding these parameters makes it clear where you can focus to enhance your approval odds.

2. How do I improve my debt-to-income ratio?

To improve your debt-to-income ratio, start by paying down existing debts, avoiding new credit card acquisitions, and boosting your income where possible. Calculate your total monthly debt payments against your gross monthly income, as this information is critical for loan applications. A lower ratio signals financial health to lenders.

3. Can I be approved for a car loan with bad credit?

Yes, while it’s more challenging, many lenders offer options for individuals with bad credit. However, expect to accept higher interest rates. Additionally, consider looking for co-signers or those willing to put down a considerable down payment to improve chances of approval.

4. How important is the loan pre-approval process?

The pre-approval process is vital as it helps you know how much you can borrow. It simplifies the buying process and makes you more attractive to sellers. It also gives you leverage in negotiations with lenders and helps streamline documentation requirements.

5. What common mistakes should I avoid during the loan application?

Avoid submitting incomplete applications and failing to provide required documentation. Other common mistakes include neglecting to shop around for the best rates or terms, assuming your income is sufficient without verification, and underestimating the importance of a good credit profile.