How to Accurately Calculate CD Interest in 2025

Understanding CD Interest Rates

When you decide to invest in a certificate of deposit (CD), understanding how to calculate **CD interest** is crucial for maximizing your returns. The **interest rates** on CDs are often higher than those on traditional savings accounts, making them an attractive option for savvy investors. In this section, we will discuss how interest rates for CDs are determined, as well as essential factors affecting **certificate of deposit interest rates**.

Factors Affecting CD Interest

Various factors influence the interest rates offered on CDs. Primarily, the prevailing economic conditions determine how **banks calculate CD interest**. For instance, in times of economic growth, banks may offer better rates to attract more deposits. Other factors include the length of the CD term, the amount deposited, and competition among banks, which plays a significant role in **comparing CD interest rates**. Understanding these factors will empower you to make informed decisions when selecting the right CD for your financial goals.

Choosing the Right CD for Interest

To optimize your investment, choosing the right CD based on its length and interest payouts is key. Some may prefer a shorter-term CD to have access to their funds sooner, whereas others might opt for long-term CDs in exchange for higher rates. **Fixed-rate CD interest calculation** typically ensures consistent returns, while variable rate CDs may fluctuate based on market conditions. Regardless of your choice, ensure you compare different offerings to find the best fit.

The Importance of Understanding APY

Annual Percentage Yield (APY) is crucial in understanding your potential earnings on CDs, as it accounts for compounding interest over time. A higher APY means better returns, so **understanding APY on CDs** is vital. Don’t just look at nominal rates; consider APY to see how different CDs compare realistically, assisting you in predicting **CD interest earnings** more accurately.

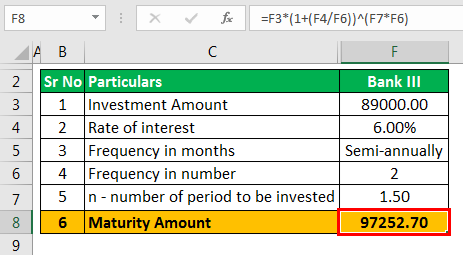

Step by Step CD Interest Calculation

Calculating **CD interest** can seem daunting, but by following a straightforward process, you can accurately determine your potential interest earnings. The **CD interest formula** often varies based on whether the interest is compounded monthly, quarterly, or annually. Below is a simplified step-by-step breakdown of the typical calculations involved.

Calculating Total Interest Earned on CDs

To calculate **total interest earned on CDs**, you first need to identify the principal amount, the interest rate, and the CD term length. Use the formula: I = P * r * t, where I is interest, P is the principal, r is the interest rate (expressed as a decimal), and t is time in years. For example, if you invest $1000 at an annual interest rate of 2% for 5 years, your interest earned would be: I = 1000 * 0.02 * 5 = $100. This straightforward formula allows investors to foresee their potential returns effectively.

Using Online CD Calculators

For an easier way to calculate **interest earnings on certificates of deposit**, consider using **online CD calculators**. These tools take the guesswork out of interest calculation and provide estimates based on various scenarios. By inputting your principal, term length, and interest rate, you can quickly see the total interest accrued. Such calculators streamline the decision-making process when evaluating your options and ensure you are making data-driven investments.

Understanding CD Maturity Date and Interest

The **CD maturity date** marks when you can withdraw your funds along with the earned interest without penalties. Knowing how the **interest accrual on CDs** works is essential. Most banks compound interest monthly or quarterly, which significantly impacts total interest earned by maturity. Understanding how **CD maturity dates** correspond with your withdrawal needs can help avoid unnecessary fees and penalties associated with early withdrawals, enhancing your overall returns.

Maximizing Interest on Your CD Investments

Maximizing interest on your CDs requires strategic planning and an understanding of available options. By effectively comparing bank offerings and utilizing various strategies, investors can significantly increase their returns from CDs. This section discusses proven methods for **maximizing CD interest** and effective investment strategies.

Strategies for Higher CD Interest Rates

One of the most effective strategies for securing better CD interest rates is laddering. This involves opening multiple CDs with different maturity dates, allowing you to take advantage of rising interest rates while accessing some cash regularly. Additionally, keep an eye on **bank promotions and CD interest**, as some institutions offer limited-time bonuses. Leveraging these strategies can enhance overall profitability from your **CD investment strategy**.

Understanding Early Withdrawal Penalties

Before you commit to a CD, it’s essential to understand the **early withdrawal penalties on CDs**. These penalties can eat into your earnings significantly if you need to access your funds before the maturity date. Ensure you read the terms carefully and consider your financial situation to avoid unnecessary fees. Familiarizing yourself with various **CD payout options** can help you navigate tax implications and effectuate a more practical approach to retirement savings.

Managing Multiple CDs Effectively

If you decide to diversify with multiple CDs, effective management is crucial. Track each CD’s maturity date and interest rates, and regularly review options for renewal. Consider your overall financial goals and liquidity needs to assess whether consolidating your CDs or splitting them further would provide optimal returns. This proactive approach enables you to adeptly **manage multiple CDs** while keeping costs and taxes minimal.

Key Takeaways

- Understanding factors affecting certificate of deposit interest rates is essential for maximizing returns on your investment.

- Step by step calculations allow for accurate forecasting of potential interest earnings, enabling informed decisions.

- Innovative strategies such as laddering can enhance your investment returns significantly.

- Be aware of early withdrawal penalties to ensure that you maintain maximum earnings on your deposits.

- Effective management while comparing various bank offerings helps in securing the best CD interest rates possible.

FAQ

1. What is a certificate of deposit?

A certificate of deposit (CD) is a type of savings account offered by banks with a fixed interest rate and fixed term. When you open a CD, you agree to keep your money deposited for a specific period in exchange for a higher interest rate than standard savings accounts.

2. How are CD interest rates determined?

CD interest rates are influenced by economic conditions, the term length of the CD, and overall competition among banks. During low inflation periods, **interest rate trends for CDs** may decline, while in stable economic growth, rates may increase.

3. What are the different interest calculation methods for CDs?

CD interest can be calculated using various methods including simple interest, compound interest, and periodic interest calculation. Most often, interest on CDs is compounded monthly or quarterly, making understanding these methods crucial to maximizing returns.

4. Can I withdraw funds from my CD early without penalties?

Typically, withdrawing funds from a CD before the maturity date invokes penalties, which can significantly impact your total interest earnings. Some banks may offer CDs with “no penalty” withdrawals, but it’s essential to read the terms carefully to avoid unexpected fees.

5. How do I find the best CD offers in 2025?

To find the **best CD interest rates**, compare various bank offerings, look for online banks that often provide better rates, check local credit unions, and utilize online resources that aggregate CD rates. Additionally, consider promotional rates that banks may offer periodically.